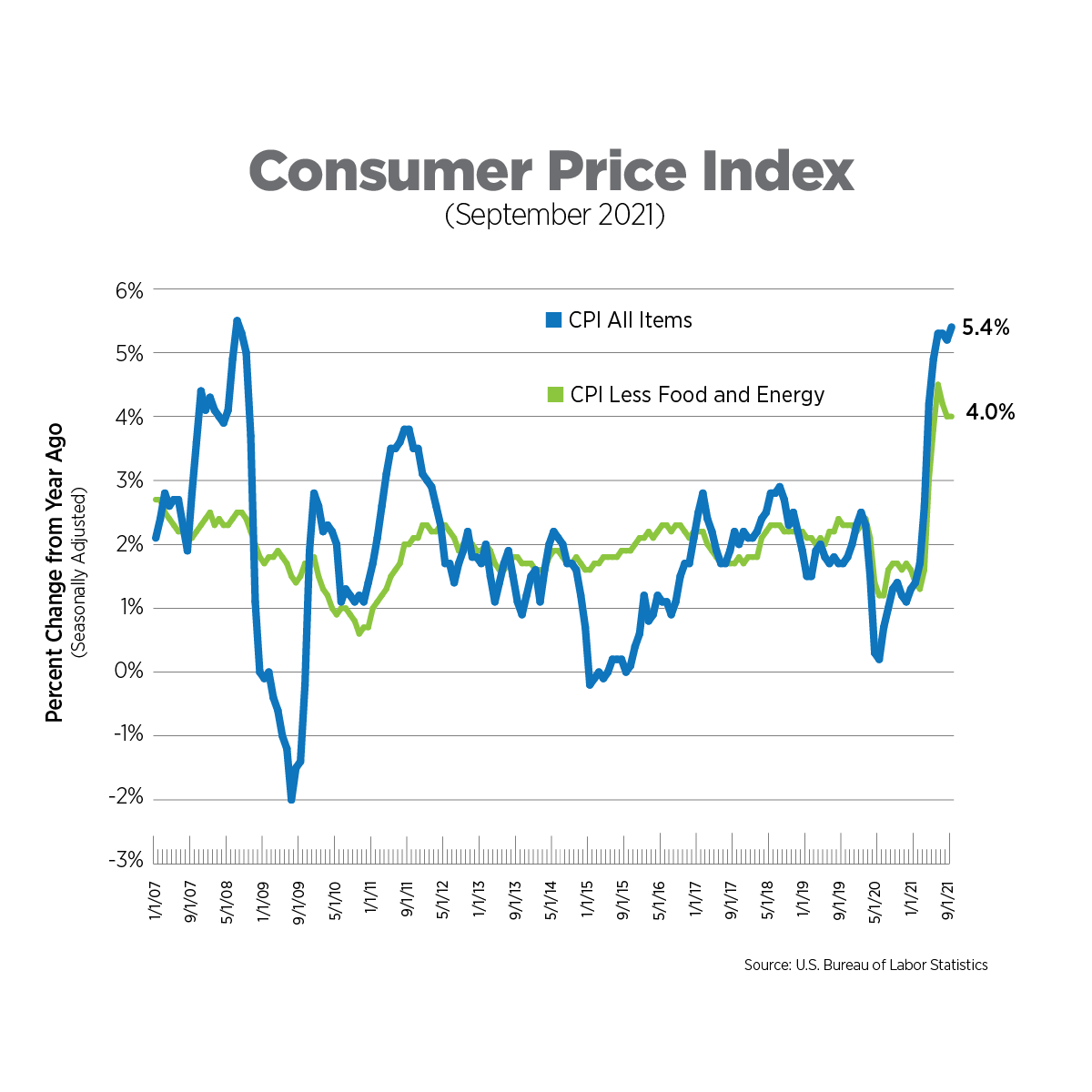

CPI, Latest Release, September 2021, 5.4%

The Consumer Price Index (CPI) rose 5.4% on a year-over-year basis, while prices excluding food and energy (core CPI) rose 4.0%, slightly above consensus forecasts. For headline CPI, energy drove price increases, up nearly 25% year-over-year. Used cars and trucks and new vehicles were still responsible for the largest year-over-year increases in core CPI, up 24.4% and 8.7%, respectively.

Monthly changes in CPI can better inform us of more current trends. Core CPI showed price increases in some categories related to the reopening of the economy beginning to ease, including airfares (down 6.4%), apparel (down 1.1%), and used cars and trucks (down 0.7%). Monthly price increases were highest for car insurance (up 2.1%), new vehicles (up 1.3%) and tobacco/smoking products (up 0.7%).

Source: US Bureau of Labor Statistics

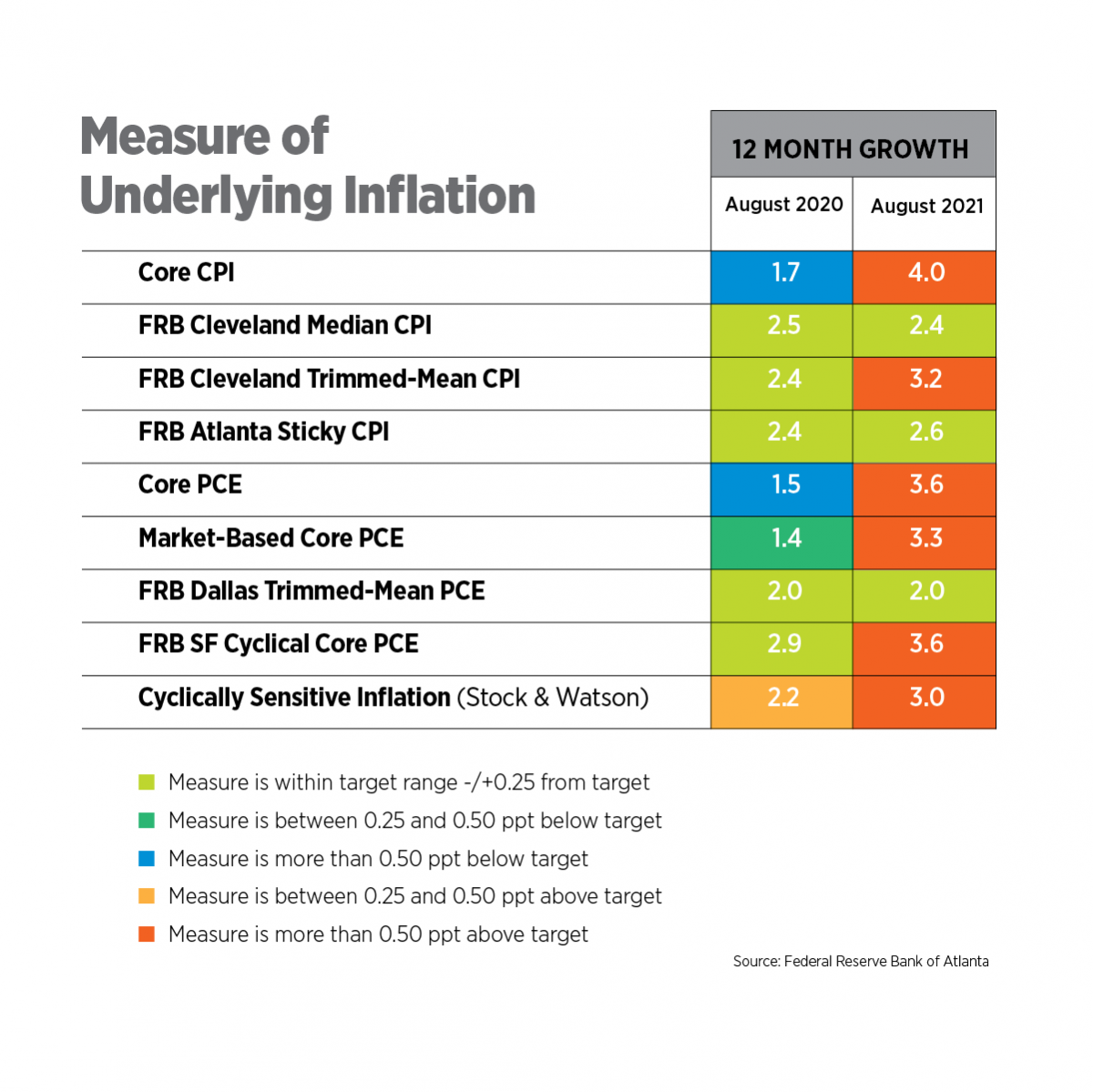

Alternative Measures of Inflation, August 2021

We have examined several alternative measures of inflation in prior Inflation Trackers, but the Atlanta Fed consolidates all of them into an Underlying Inflation Dashboard, updated monthly. There was very little change from July to August in terms of the number of measures at one-half a percentage point or more above their target, but the San Francisco’s Fed Cyclical Core PCE experienced the greatest month-to-month increase. Cyclical components, such as child-care costs, are more sensitive to overall economic conditions versus cyclical components, which are more closely tied to a particular industry.

Source: Federal Reserve Bank of Atlanta

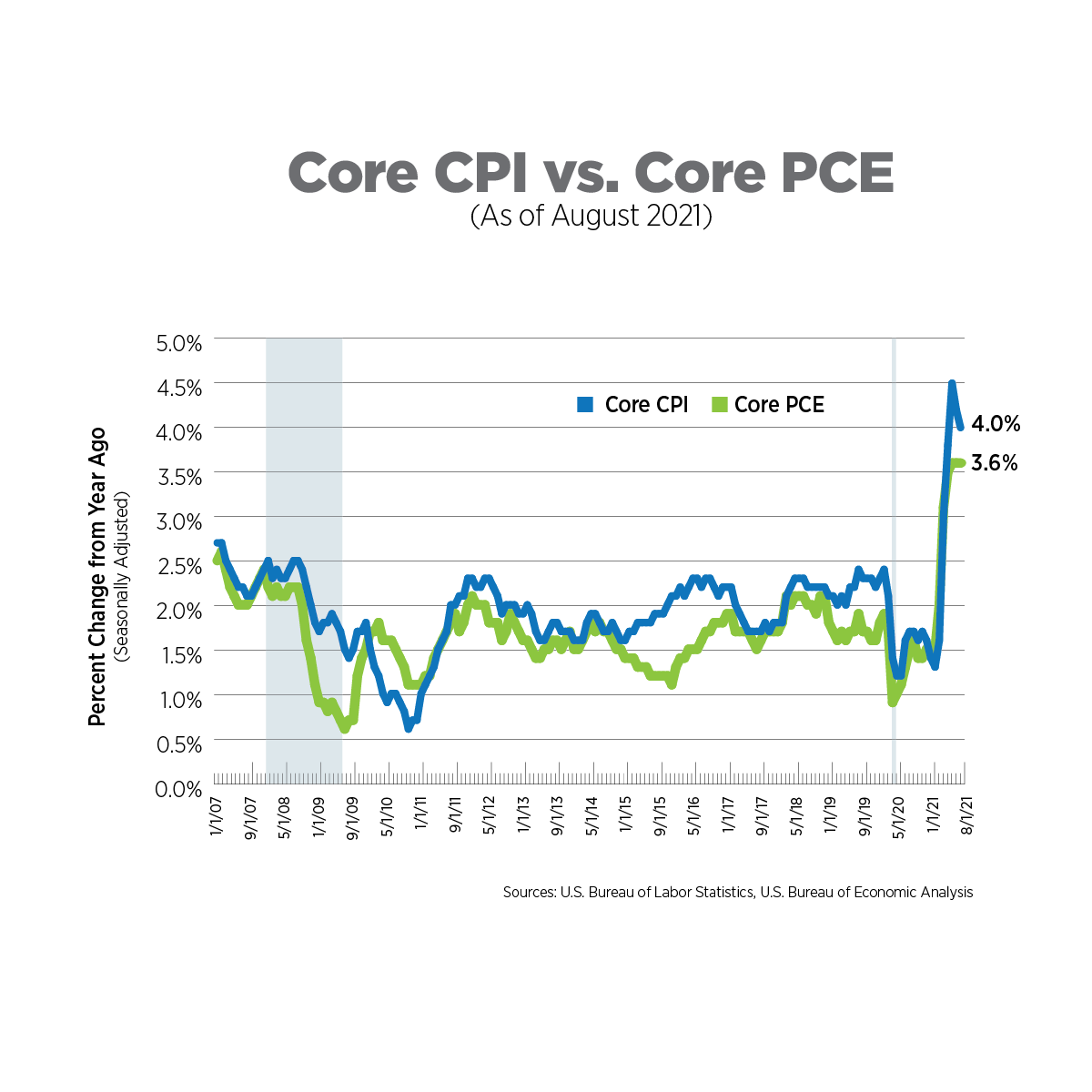

Alternative Measures of Inflation, August 2021

The Personal Consumption Expenditures (PCE) Index is the measure of inflation the Federal Reserve Bank uses in its policy decisions. It is produced by the Bureau of Economic Analysis and uses different formulas, different weights and has a different scope compared to the Bureau of Labor Statistics’ (BLS) CPI.

In August, core PCE increased 3.6 percent year-over-year for the third consecutive month, meaning it is on track to achieve the Fed’s long-term target of 2% by the end of this year. In fact, the Fed could make a decision on when to start easing bond purchases at its November meeting, with mid-2022 targeted as a deadline in prior discussions. The tapering could cause upward pressure on interest rates. In terms of the Fed raising interest rates, most analysts and economists do not expect that to occur until late 2022/early 2023, a position fully supported right now by the weakening labor market.

Sources: U.S. Bureau of Labor Statistics, U.S. Bureau of Economic Analysis

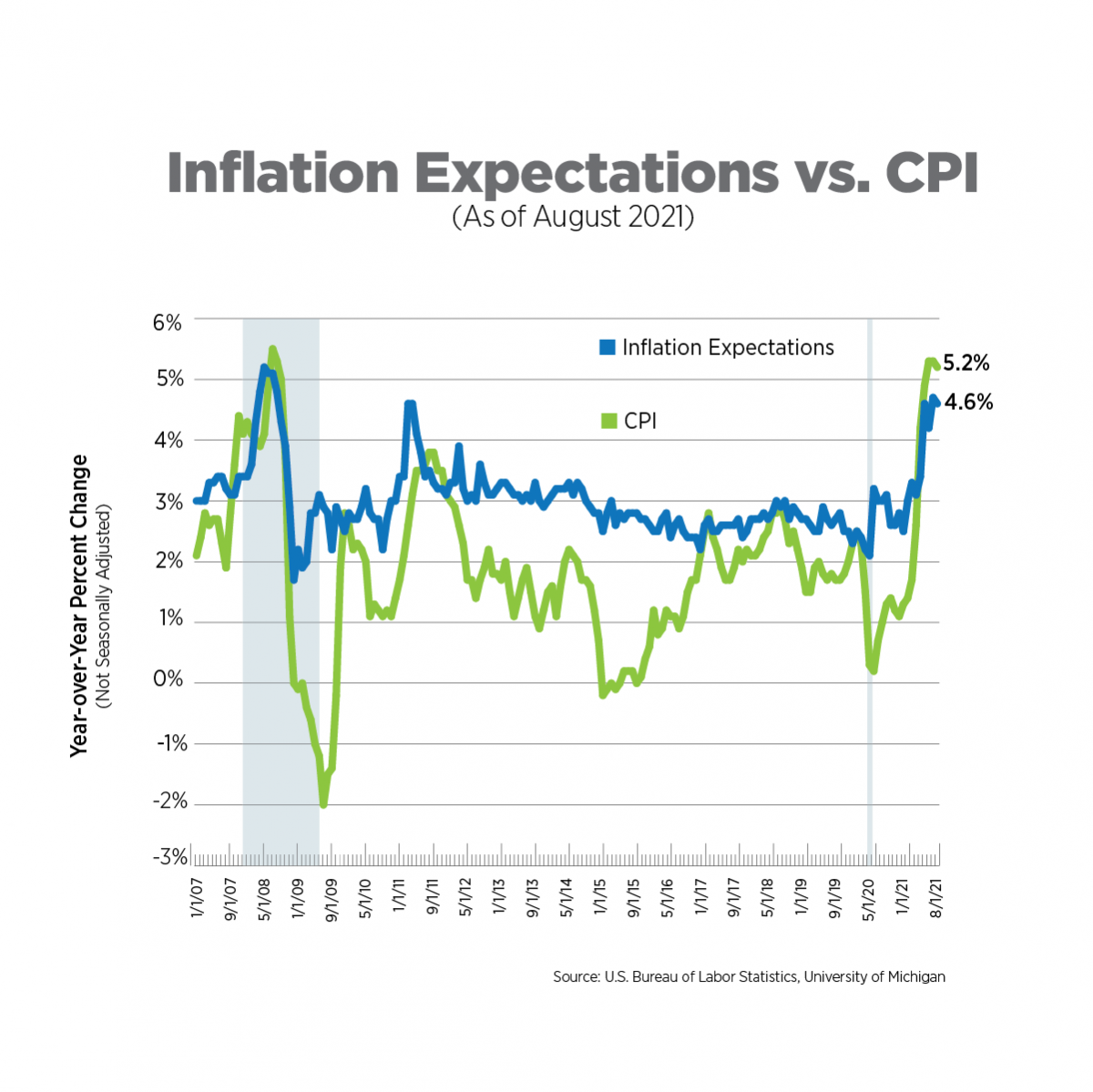

Inflation Expectations, August 2021

The Fed tracks 21 different measures of inflation expectations. The measure presented in the chart below is from the University of Michigan’s Consumer Sentiment Survey. Expectations remained elevated in the most recent reading but are largely in line with those during the Great Recession. Expectations are often described as a self-fulfilling prophecy, indicating to producers a level of price increase consumers will accept if they move forward with purchases. Expectations can also put further pressure on wages as those same consumers demand more pay to cover price increases.

Source: U.S. Bureau of Labor Statistics; University of Michigan

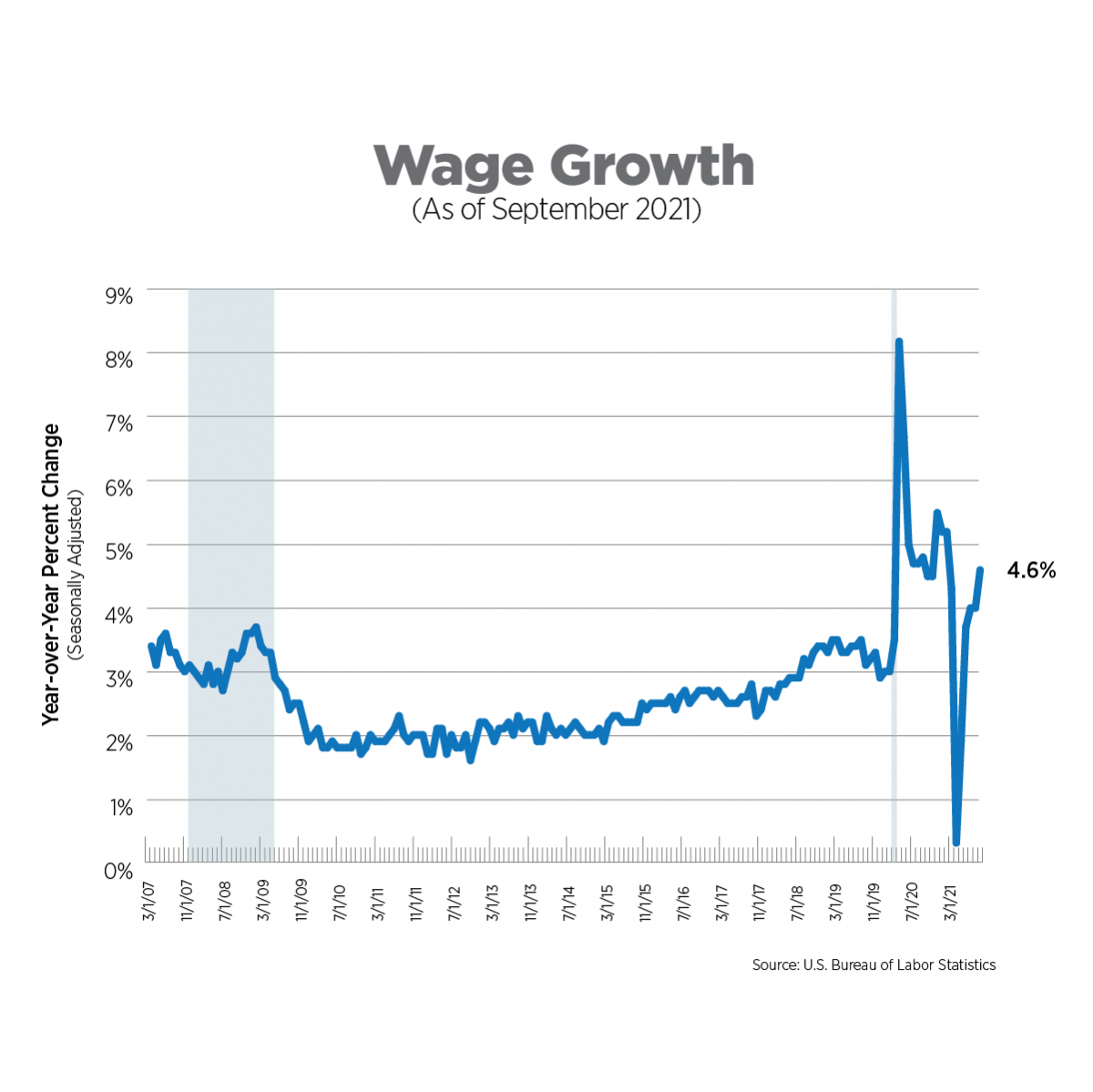

Wage Growth, September 2021

Wage growth remained robust in September, increasing 4.6% on a year-over-year basis as employers tried to attract workers amid an abundance of job openings. In the September Employment Situation Summary, the Bureau of Labor Statistics warned that wage growth figures may not be accurately reflecting conditions in the market due to the volatile swings in employment since the pandemic began as well as the wide variations in wages among industries. Still, the near-peak number of job openings, as well as the record-breaking number of workers quitting their jobs, signal continued strong wage growth.

Source: U.S. Bureau of Labor Statistics

What to Watch in the Next Month

By and large, the Fed is standing by its estimation that inflation will be temporary. The International Monetary Fund also believes inflationary pressures will ease in 2022 but warned in its most recent World Economic Outlook report (released October 12, 2021) that there is so much uncertainty around inflation that Central Banks across the world, including the Fed, need to be prepared to tighten monetary policy sooner than expected.

The Fed meets on November 2-3. Importantly, the meeting occurs before the October jobs report release, meaning the Fed will be relying on the weak September report to evaluate the labor market as well as other labor market measures like unemployment claims. If the Fed believes the labor market still needs more time to recover, it may continue to hold off on tightening monetary policy.

Next Tracker: November 10, 2021